This is part 2 of a series on building grounded AI for payment systems. Part 1 made the case that payments need grounded AI, not a generic LLM guessing from training data. This post covers the pattern that delivers the grounding.

In the previous post I argued that a generic LLM has payment vocabulary but not payment context. The practical question is how to give it that context. This is where Retrieval-Augmented Generation becomes interesting.

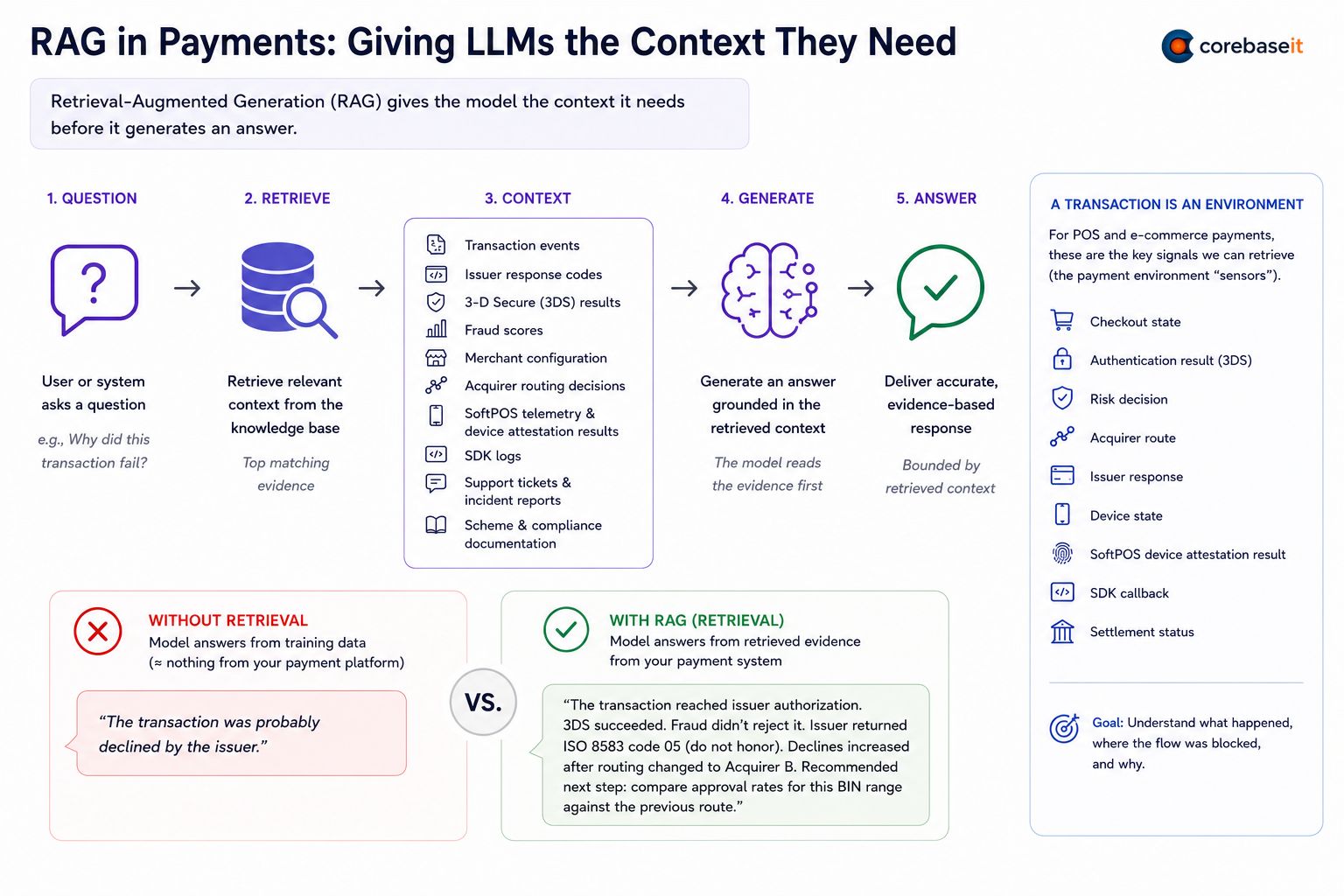

RAG has an intimidating name for a simple idea: before the model answers, it retrieves relevant context. Lewis et al. introduced the pattern in 2020, pairing a language model with a retrieval mechanism so that generation is grounded in fetched evidence instead of parametric memory alone.

That one step changes the role of the LLM. Without retrieval, the model answers from what it absorbed during training, which for your payment platform is approximately nothing. With retrieval, the model first reads the evidence:

- transaction events

- issuer response codes

- 3-D Secure (3DS) results

- fraud scores

- merchant configuration

- acquirer routing decisions

- SoftPOS telemetry and device attestation results

- SDK logs

- support tickets and incident reports

- scheme and compliance documentation

Then it generates an answer bounded by that context.

The ENWAR translation

The pattern I want to borrow comes from a different domain entirely. ENWAR (Nazar et al., 2024) is a RAG-empowered multi-modal LLM framework for wireless environment perception. Its authors faced the same problem payment engineers face: an LLM that knows the vocabulary of a technical domain but not the live state of a specific system.

Their solution does not ask the LLM to guess the wireless environment. It transforms GPS, LiDAR, and camera inputs into structured textual context, chunks and embeds that context into a domain knowledge base, retrieves the relevant pieces at question time, and only then lets the LLM generate situational awareness. In their evaluation, the grounded system identified vehicle positions, obstacles, and line-of-sight conditions that vanilla models described only superficially.

That pattern translates surprisingly well to payments. In wireless systems, the question may be “is there line-of-sight between two vehicles?” In payments, the equivalent question is “where was the payment flow blocked?”

A transaction is also an environment. It has signals, paths, obstacles, and context. The modalities map almost one to one:

| ENWAR input | Payment equivalent | What it tells you |

|---|---|---|

| GPS | Transaction metadata | Where, when, how much, which merchant, which channel |

| LiDAR | Device and infrastructure telemetry | What the terminal, SDK, network, or app observed |

| Camera | Behavioral and support context | What the user, merchant, or support conversation reveals |

| Wireless knowledge base | Payment knowledge base | Scheme rules, risk logic, SDK docs, incident history |

| Line-of-sight analysis | Payment path analysis | Can the flow complete without blockage? |

| Obstacle detection | Failure cause detection | What prevents approval, capture, or settlement? |

For a POS or e-commerce payment, the retrievable signals include the checkout state, the authentication result, the risk decision, the acquirer route, the issuer response, the device state, the SoftPOS device attestation result, the SDK callback, and the settlement status. Each one is a sensor reading from the transaction environment.

Two answers to the same question

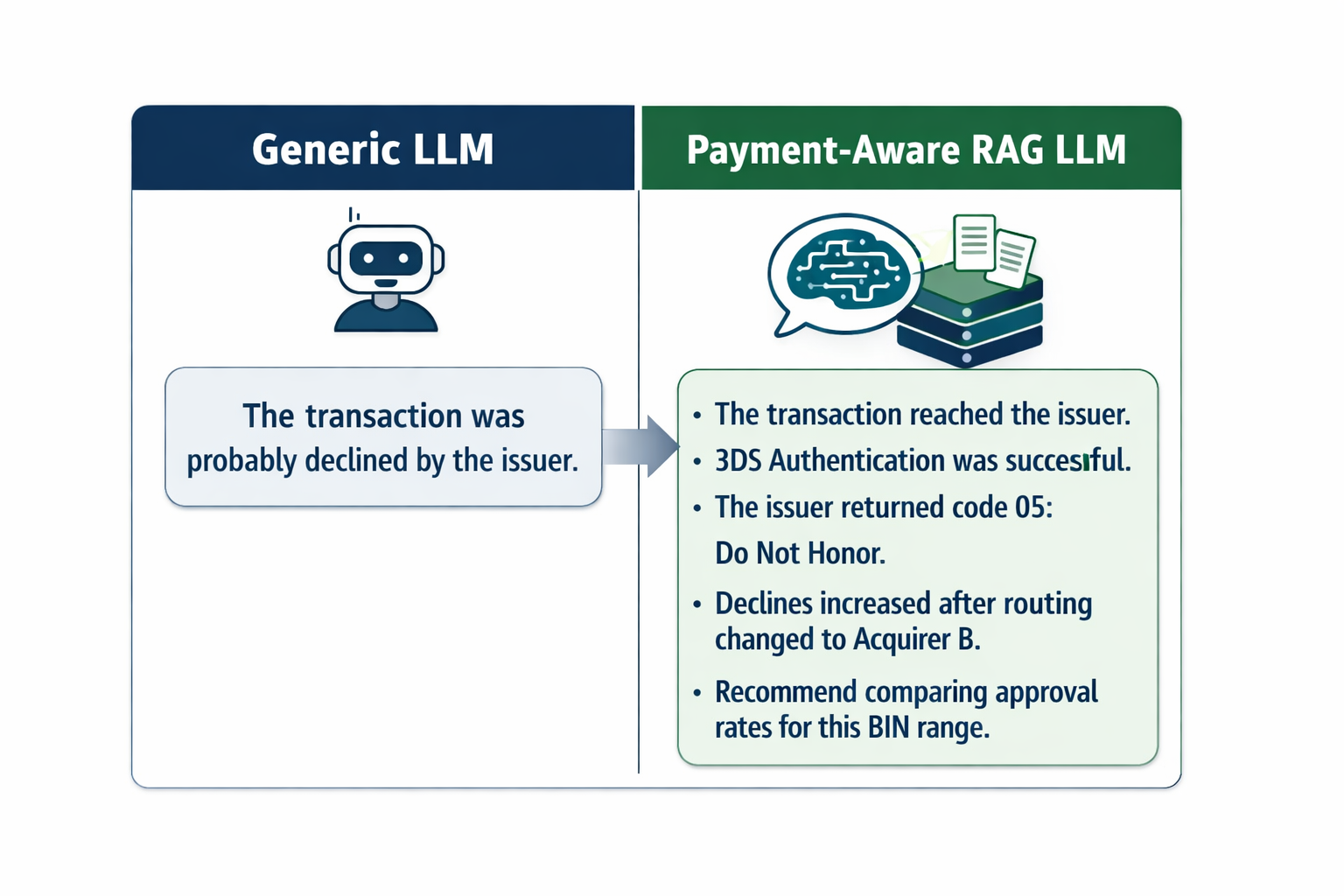

The difference this makes is easiest to see side by side. Ask why a transaction failed.

A generic LLM says:

“The transaction was probably declined by the issuer.”

A payment-aware RAG system, answering from retrieved evidence, can say:

“The transaction reached issuer authorization. 3DS authentication succeeded. The fraud engine did not reject it. The issuer returned ISO 8583 response code 05 (do not honor). Similar declines increased after routing changed to Acquirer B. Recommended next step: compare approval rates for this BIN range against the previous route.”

The second answer is hypothetical, but every claim in it traces to a retrievable record: an authorization event, a 3DS result, a risk engine output, a routing change log. Code 05 is a deliberately uninformative response — issuers use it precisely when they don’t want to disclose the reason — which is exactly why the surrounding evidence matters more than the code itself.

The fluency of the two answers is identical. The difference is that the second one is connected to evidence, and that connection is what makes it usable in a support case, a risk review, or an incident report.

The architectural direction

For me, this is the right architectural direction for AI in payments. The LLM stays out of the authorization path. It does not guess decline reasons from training data, and it does not replace certified payment logic. It operates as a grounded intelligence layer around the payment lifecycle: one that can retrieve, reason, explain, and assist while the deterministic engine keeps executing transactions.

In POS and e-commerce, the question that matters is shifting. It is no longer “can the LLM answer?” Any current model can produce an answer. The question is “what context did it use before answering?” That makes context retrieval an architectural concern, the same way I argued that prompts in payment systems are configuration contracts, not chat messages.

Part 3 makes this concrete: the use cases where a grounded layer earns its keep in POS, SoftPOS, and e-commerce, from merchant support and decline explanation to fraud review and audit support.

References

- A. M. Nazar, A. Celik, M. Y. Selim, A. Abdallah, D. Qiao, A. M. Eltawil, “Enwar: A RAG-empowered Multi-Modal LLM Framework for Wireless Environment Perception,” arXiv:2410.18104, 2024.

- P. Lewis et al., “Retrieval-Augmented Generation for Knowledge-Intensive NLP Tasks,” NeurIPS 2020, arXiv:2005.11401.