Online vs Offline EMV Transactions: Why Offline Still Matters

In EMV payments, “online” and “offline” do not mean secure and insecure. They describe where the transaction decision is made, which risk controls are available, and how much the issuer can participate in real time.

In an online EMV transaction, the terminal sends an authorization request to the issuer through the acquirer and payment network. In an offline EMV transaction, the terminal and card can complete the transaction without waiting for an issuer response, using EMV rules, card parameters, terminal parameters, cryptographic checks, and risk limits.

Most modern card-present payment environments are biased toward online authorization. That makes sense: issuers want real-time fraud scoring, balance checks, sanctions controls, token controls, card status updates, and authorization decisioning. But offline EMV is not a legacy curiosity. It is part of the design language of EMV, and it still matters in places where payment acceptance must continue even when connectivity is imperfect.

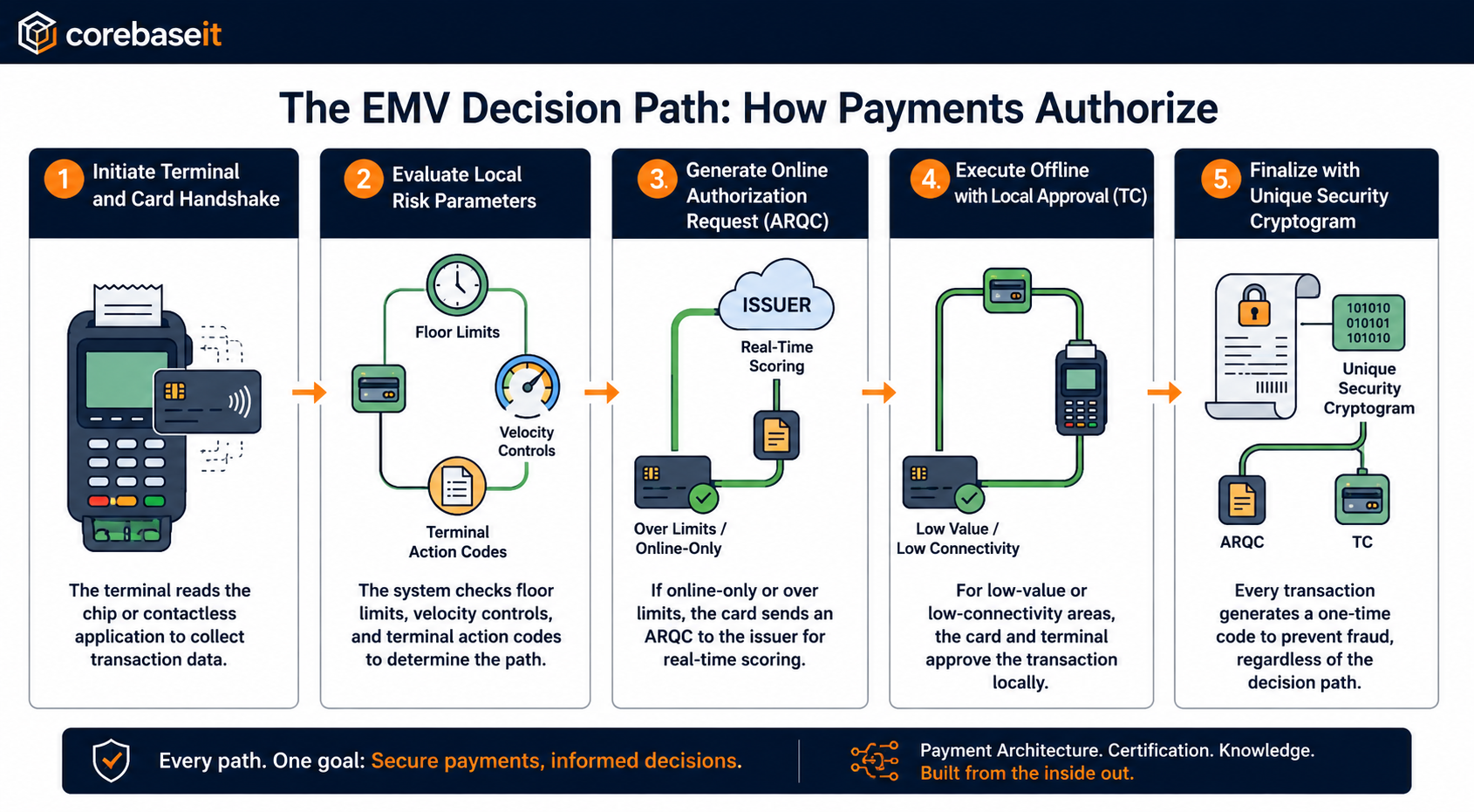

The diagram above traces the standard EMV decision path. After the terminal and card exchange transaction data, local risk parameters — floor limits, velocity controls, and terminal action codes — determine whether the transaction goes online with an ARQC or completes offline with a TC. Both paths still produce a one-time security cryptogram. The sections below walk through each branch in more detail.

The short version

Online EMV is issuer-led. Offline EMV is terminal-and-card-led.

In an online transaction, the card generates an Authorization Request Cryptogram, or ARQC, which is sent to the issuer for validation. AWS Payment Cryptography describes ARQC as a cryptogram generated by an EMV chip card to validate both transaction details and the use of an authorized card; it incorporates data from the card, the terminal, and the transaction itself (AWS Payment Cryptography).

In an offline transaction, the terminal and card make the decision locally. The transaction may be approved with a Transaction Certificate, declined with an Application Authentication Cryptogram, or sent online when the risk rules say the issuer should be involved. The key point is that EMV was designed so the card and terminal can participate intelligently in the decision, rather than behaving like a passive magnetic-stripe read.

EMVCo explains that EMV chip technology generates a one-time security code for every transaction, and that this code helps the issuer and point-of-sale terminal authenticate the card (EMVCo Contact Chip). EMVCo also states that contactless EMV transactions generate a one-time use security code for every transaction, whether the consumer taps a card or an NFC-enabled mobile device (EMVCo Contactless Chip).

What happens in an online EMV transaction?

An online EMV transaction follows the normal card-present authorization path. The terminal reads the chip or contactless application, performs local EMV processing, collects transaction data, and asks the card to generate an ARQC. That ARQC is then carried in the authorization message toward the issuer.

The issuer or issuer processor validates the ARQC by reconstructing the cryptogram inputs and comparing the expected value with the value received from the transaction. AWS describes this backend process as recreating the cryptogram using the same inputs and comparing it to the value provided by the transaction, similar to how a MAC is validated (AWS Payment Cryptography).

Once the issuer makes the authorization decision, it can return an approval or decline, and in many implementations it may also return issuer authentication data or issuer scripts. In simple terms, online EMV gives the issuer the best visibility and control at the moment of purchase.

That is why many markets and acceptance environments configure terminals as online-first or online-only. Visa’s U.S. online-only terminal configuration, for example, says the terminal floor limit must be set to zero and that the terminal action code for online processing must be configured so that, unless the terminal has already determined a decline condition, the transaction is forced online (Visa Minimum U.S. Online Only Terminal Configuration).

For SoftPOS, mPOS, e-commerce-adjacent card-present flows, and many modern acquiring stacks, online authorization is usually the safest default. It allows the issuer to check the account, validate the cryptogram, apply dynamic risk scoring, and react to fraud signals immediately.

What happens in an offline EMV transaction?

Offline EMV shifts part of the decision closer to the point of interaction. The terminal and card evaluate whether the transaction can be approved without an issuer response. That decision is not arbitrary. It is driven by parameters such as terminal floor limits, terminal capabilities, card risk parameters, cardholder verification results, offline authentication support, and terminal risk management.

Terminal risk management includes checks such as whether the transaction amount exceeds the terminal floor limit, whether the transaction is selected randomly for online processing, and whether velocity limits indicate that too many consecutive offline transactions have occurred (CardContact OpenSCDP). These checks populate the Terminal Verification Results, or TVR, which then influences terminal action analysis and the request made to the card.

Offline does not mean “no security.” In fact, the security model is the reason offline EMV is possible. The chip can generate transaction-specific cryptograms, the terminal can apply risk rules, and the card can enforce issuer-defined limits. EMVCo’s description of chip payments highlights that transaction cryptograms are unique and cannot be reused, which is a fundamental difference from traditional magnetic-stripe data (EMVCo Contact Chip).

The trade-off is that the issuer does not get the same real-time visibility it gets with online authorization. An offline approval may not know the current account balance, the latest fraud score, a just-blocked card status, or a recent issuer-side rule change. That is why offline approvals are usually constrained by low limits, velocity controls, merchant category rules, scheme rules, and regional policy.

Online-only does not eliminate offline thinking

A common misunderstanding is that if a terminal is online-only, offline EMV no longer matters. In reality, online-only configurations still depend on EMV concepts such as floor limits, terminal action codes, issuer action codes, TVR bits, cryptograms, and fallback behavior.

Visa’s online-only configuration document is a good example. It explains that a zero floor limit and specific terminal action code settings are used to force online processing, and it also notes that U.S. EMV cards and online-only terminals typically do not support offline approvals (Visa Minimum U.S. Online Only Terminal Configuration). That does not remove EMV decisioning. It configures the decisioning path toward ARQC and issuer authorization.

The same document also discusses deferred authorization for temporary connectivity issues. In that model, the merchant or acquirer may defer the ARQC authorization request until connectivity is restored, but if the deferred authorization is later declined, the transaction must not be cleared or settled (Visa Minimum U.S. Online Only Terminal Configuration).

This distinction is important for payment architects. Offline EMV approval, online-only authorization, and store-and-forward authorization are related ideas, but they are not the same thing. A proper design must be clear about who is taking the risk, what cryptogram is generated, when the issuer receives the transaction, and what happens if the issuer later declines.

Why offline still matters

Resilience at the edge

Payment acceptance does not always happen in perfect network conditions. Think of parking meters, vending machines, taxis, ferries, aircraft, outdoor events, rural merchants, temporary venues, or stores with intermittent broadband. If the network disappears, the business still has to decide whether to stop selling or accept some controlled risk.

Offline capability gives the ecosystem a way to keep low-risk commerce moving. It does not mean every transaction should be approved offline. It means the system has a structured way to decide what can proceed, what must go online, and what must be declined.

Speed in high-throughput environments

Transit is the classic example. A gate cannot behave like a slow checkout lane. Riders expect to tap and move. In these environments, the acceptance design often combines fast local decisioning, risk limits, delayed processing, and back-office aggregation.

EMVCo notes that EMV chip technology supports not only credit and debit card payments but also use cases such as loyalty programmes and transit ticketing (EMVCo Contact Chip). That broader scope matters because transit and unattended acceptance push payment systems toward designs where latency and availability are product requirements, not just technical metrics.

Inclusion and reliability

In a globally deployed payment system, not every market has the same network quality, terminal estate, issuer capability, or merchant profile. Online-only may be the right model for one country, one scheme, or one product. It may be less practical in another acceptance environment.

Offline EMV gives issuers, acquirers, schemes, and merchants a vocabulary for controlled acceptance when real-time connectivity cannot be assumed. That vocabulary includes offline authentication, CVM support, floor limits, terminal risk management, velocity limits, and action-code-based decisioning.

Certification and implementation reality

Even if a product strategy says “always online,” the engineering team still has to understand the EMV mechanics. Level 2 kernels, terminal parameters, payment-system rules, contactless kernels, and Level 3 certification scenarios all depend on the correct behavior of terminal/card decisioning.

EMVCo states that contactless acceptance is based on EMV Chip, EMV Contactless, and EMV Contactless Kernel Specifications, and that each global payment system has its own Book C-X contactless kernel specification (EMVCo Contactless Chip). For a terminal vendor, SoftPOS provider, acquirer host, or certification team, those kernel behaviors are not abstract. They decide whether a transaction requests ARQC, approves offline, declines offline, or follows a scheme-specific path.

Practical examples

A supermarket with stable connectivity

For a supermarket in a mature market, online EMV is usually the expected path. The terminal asks the card for an ARQC, the acquirer sends the authorization request, and the issuer approves or declines in real time. The merchant benefits from issuer decisioning, and the issuer gets the best opportunity to manage fraud and account risk.

A vending machine in a weak-coverage area

For a low-value unattended transaction, it may be commercially reasonable to accept a limited amount of offline or deferred risk. The system can enforce limits per card, per terminal, per day, or per merchant. If the parameters are too permissive, fraud and insufficient-funds exposure increase. If they are too strict, acceptance drops.

A transit gate at rush hour

The product requirement is not simply “authorize a card.” The requirement is “let the rider pass quickly while keeping aggregate risk under control.” That often leads to a hybrid model: fast local checks at the gate, back-office risk controls, delayed authorization or aggregation logic, and clear rules for blocking cards that later fail authorization.

A SoftPOS application

For a mobile acceptance application, online-only is often the right model because the device is connected, the acquirer wants centralized risk control, and scheme rules may limit offline behavior for that acceptance channel. But the SoftPOS team still needs to understand EMV offline concepts because kernel configuration, CVM support, ARQC generation, offline decline behavior, and deferred authorization rules can all appear during certification and production edge cases.

The risk question: who carries the exposure?

The technical difference between online and offline EMV quickly becomes a business question: who takes the risk if the transaction later turns out to be bad?

With online authorization, the issuer makes the decision in real time, subject to scheme rules and liability frameworks. With offline approval or deferred authorization, the merchant or acquirer may carry more exposure because the issuer did not approve the transaction before goods or services were delivered. Visa’s deferred authorization guidance explicitly notes that merchants assume “open to buy” risk, including insufficient funds risk, and recommends controls such as velocity checking and cumulative amount limits on repeat purchases (Visa Minimum U.S. Online Only Terminal Configuration).

That is why offline should never be treated as a simple performance optimization. It is a risk product. It needs limits, monitoring, exception handling, dispute logic, reconciliation rules, and clear ownership between merchant, acquirer, processor, network, and issuer.

Design principles for modern payment architects

Prefer online when the issuer should decide

If the transaction needs real-time balance checking, fraud scoring, issuer authentication, card status checks, or account controls, online authorization should be the default. This is especially true for higher-value transactions, new merchants, risky verticals, and acceptance devices with reliable connectivity.

Keep offline tightly scoped

Offline should be allowed only where the commercial need justifies the risk. Good candidates are low-value, high-throughput, or connectivity-constrained environments where the cost of declining legitimate customers is higher than the controlled risk of accepting limited offline exposure.

Treat deferred authorization separately

Store-and-forward is not the same as an EMV offline approval. A deferred transaction may capture an ARQC and send it later, but the merchant still needs rules for what happens if the issuer declines. The product, legal, operations, and reconciliation teams must all understand that lifecycle.

Certify the edge cases, not only the happy path

Payment systems fail at the boundaries: no host response, weak network, terminal parameter mismatch, unsupported CVM, expired keys, contactless kernel differences, duplicate tap, transaction reversal, failed clearing, or issuer decline after deferred submission. These scenarios should be part of the certification and operational test plan, not afterthoughts.

Make the risk visible

If offline or deferred authorization is supported, build reporting around it. Track offline approvals, deferred approvals, deferred declines, reversals, clearing failures, repeat PAN or token attempts, terminal-level exposure, and merchant-level exposure. A risk feature that is not measured will eventually become an operations problem.

Final thought

Online EMV is the dominant model because it gives issuers real-time control. Offline EMV still matters because payment systems live in the real world: networks fail, terminals move, transit gates need speed, unattended devices need autonomy, and global acceptance cannot assume perfect connectivity.

The best architecture is not “online versus offline.” It is a clear decision framework: online where issuer control is required, offline only where the risk is bounded, and deferred authorization only when the operational and liability model is understood.

For payment teams building POS, SoftPOS, acquirer processing, or certification workflows, offline EMV is still worth understanding. Even when you configure the product to go online every time, the EMV offline model explains many of the parameters, cryptograms, and edge cases that decide what actually happens at the terminal.

For a deeper dive: Online/offline decisioning, deferred authorization, and store-and-forward are covered in Point-of-Sale Systems Architecture: A Practical Guide to Secure, Certifiable POS Systems — Chapter 14: Offline and Store-and-Forward Implementation, plus the EMV kernel and authorization lifecycle chapters earlier in the book.

Further Reading

- Offline EMV vs Store-and-Forward: Two Different Mechanisms, One Confusing Name — companion post on this site; clarifies TC vs ARQC vs deferred authorization

- EMV Cryptograms: How ARQC Prevents Fraud — ARQC generation, validation, and the online authorization path

- EMV for Developers — EMV fundamentals from a developer-centric perspective

- EMVCo: EMV Contact Chip — one-time transaction codes, offline and online cryptogram paths

- EMVCo: EMV Contactless Chip — contactless kernels and scheme-specific Book C-X specifications

- Visa: Minimum U.S. Online Only Terminal Configuration — zero floor limit, forced online processing, deferred authorization rules

- EMV Migration Forum: Merchant Processing During Communications Disruptions — EMV offline authorization vs deferred authorization vs force-post

- AWS Payment Cryptography: ARQC validation — issuer-side cryptogram reconstruction and MAC validation

- CardContact OpenSCDP: Terminal Risk Management — floor limits, random online selection, velocity checks, and TVR

- Worldpay: Deferred Authorisation — acquirer-side deferred online authorization when connectivity returns

- Adyen: Offline payments — practical PSP implementation of offline and store-and-forward controls

- EMVCo Book 3: Application Specification — Terminal and Card Action Analysis, GENERATE AC, floor limits, and action codes

- D. Basin et al., “The EMV Standard: Break, Fix, Verify” — formal security analysis of offline vs online authorization models