Reversal. Refund. Chargeback. Three words every payment professional uses — and three concepts that are routinely conflated, even inside the industry. They sound interchangeable because they all describe “money going back to the cardholder,” but they are not.

Each operates at a different point in the settlement lifecycle, under a different protocol, with radically different timing and liability implications for merchants, acquirers, issuers, and cardholders. Treating them as synonyms leads to reconciliation errors, misconfigured terminals, incorrect dispute handling, and — frequently — unrecovered revenue.

This post breaks down what each one actually is, where it lives in the transaction lifecycle, and why the distinction matters at the architectural level.

The Settlement Boundary: The Line That Defines Everything

Before examining each mechanism individually, it is worth anchoring the mental model around a single concept: the settlement boundary.

At the acquirer host, every authorized transaction eventually crosses from a pending state into a settled state. This typically happens at batch close — the moment the acquirer cuts the day’s authorizations and submits them for clearing into the scheme. Before batch close, nothing has actually moved; the funds are held, not transferred. After batch close, the money is in motion through the scheme toward the issuer, and eventually back to the merchant’s account.

This boundary is what separates a reversal from a refund, and what elevates a dispute into a chargeback. Everything else — the message type, the timing, the liability model — flows from where the transaction sits relative to that line.

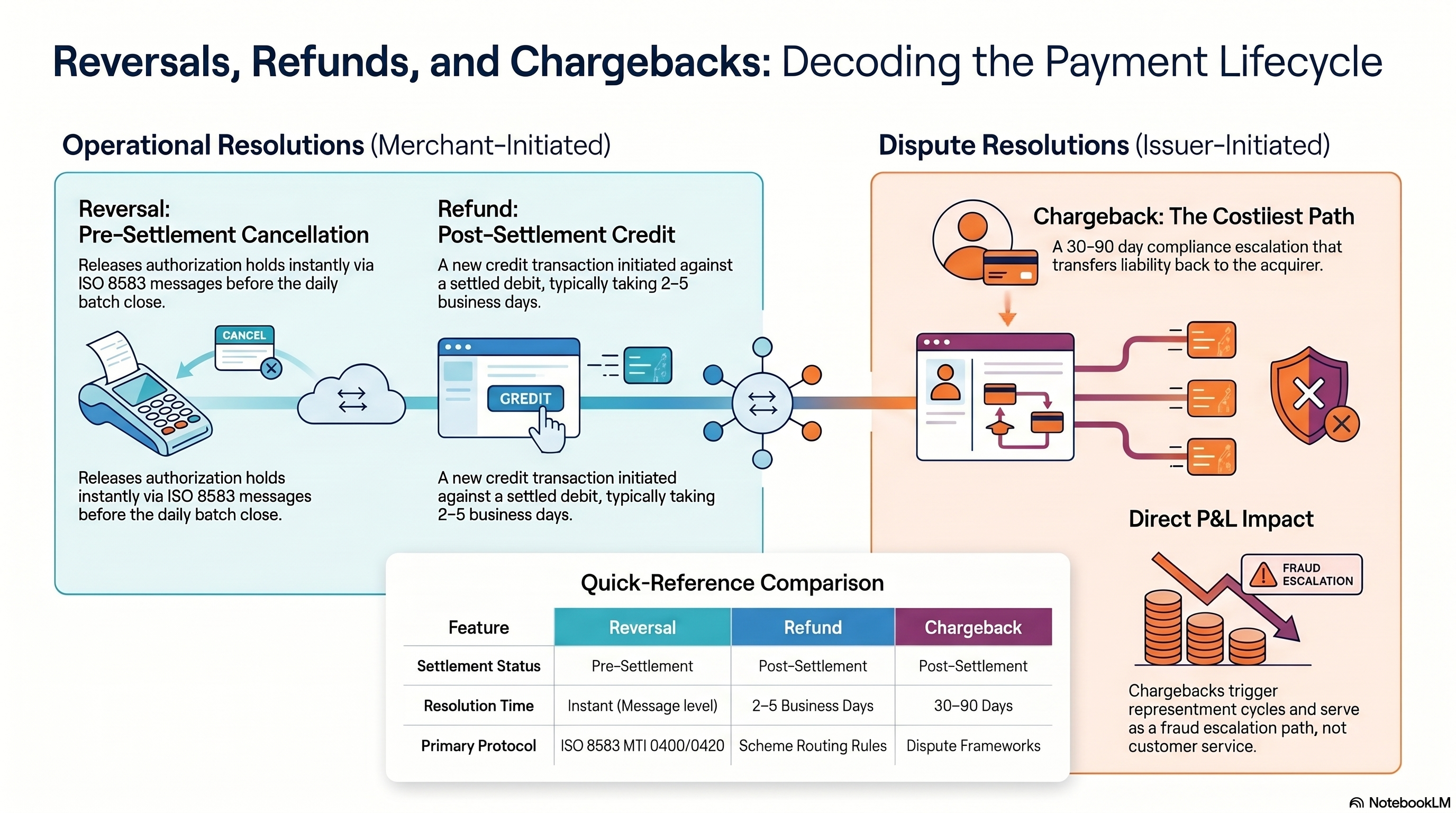

1. Reversal: A Pre-Settlement Cancellation

A reversal is a cancellation that happens before the authorization has settled. It is the cleanest, cheapest, and fastest way to undo a transaction — because no funds have moved yet.

In ISO 8583 terms, a reversal is an MTI 0400 (reversal request) / 0420 (reversal advice) message exchanged between the terminal (or acquirer) and the issuer. It instructs the issuer to release the authorization hold and restore the available balance on the card.

Reversals are generated for a range of legitimate operational reasons:

- The cardholder cancels at the terminal after approval but before printing the receipt.

- The terminal times out waiting for an issuer response and must unwind the hold.

- A duplicate authorization was submitted due to retry logic or network instability.

- A partial authorization was approved, and the merchant elects to void the entire amount.

- An EMV transaction failed at the CDA/ARPC verification step after the issuer had already approved the ARQC.

Partial Reversals and EMV

In EMV environments, partial reversals are equally critical. If the card was authorized for one amount but the final transaction settles for a lower amount — common in fuel, hospitality, and pre-authorization flows — the merchant must reverse the delta. If the authorized amount is not reconciled with the final transaction amount before batch close, the acquirer carries liability exposure for the unreleased hold, and the cardholder sees an inflated pending charge that may never clear cleanly.

Instant at the Message Level, Not Always at the Card

A reversal is instant at the message level — the 0400 is acknowledged within the same session. But the issuer-side hold release is a separate operation inside the issuer’s authorization system and may lag by hours, depending on issuer batch cycles, available-balance refresh intervals, and scheme posting rules. Engineers building customer-facing UX on top of reversals should account for this delta: the reversal succeeded at the protocol layer well before the cardholder sees the balance restored in their banking app.

2. Refund: A Post-Settlement Credit Transaction

A refund is fundamentally different. Once an authorization has cleared and settled, there is no “undo.” The original debit has already moved through the scheme, through the acquirer, and into the merchant’s settlement account. There is no hold left to release.

To return funds to the cardholder, the merchant must initiate a new credit transaction against the original PAN — a return, in scheme terminology. This is a distinct message flow, not a modification of the original authorization:

- It carries its own STAN, RRN, and authorization path.

- It is subject to scheme routing rules, interchange, and fee structures.

- It is reported in clearing and settlement as an independent item, linked to the original transaction only by reference data (original RRN, original transaction date).

- It typically takes 2–5 business days end-to-end, because it must traverse the full clearing and settlement cycle — batch close at the acquirer, network presentment, issuer posting, and cardholder statement refresh.

A refund is, architecturally, just another transaction moving in the opposite direction. It is a credit, not a reversal. And because it is a new transaction, it must pass the same risk, compliance, and validation checks as any other scheme message — which is why refunds can be declined, can fail fraud screens, and can be delayed by issuer-side controls.

Why the Distinction Matters Operationally

Merchants who conflate reversals and refunds end up with two predictable classes of bug:

- Reversals attempted after settlement — the 0400 is rejected because the original authorization no longer exists in the issuer’s pending state. The merchant must reissue the request as a refund, often after customer-support escalation.

- Refunds issued when a reversal would have been valid — the cardholder waits 3–5 business days for funds they could have seen restored the same day, generating avoidable support tickets and chargeback risk.

The correct engineering rule is simple: if batch close has not occurred, reverse; otherwise, refund. Terminal software, POS middleware, and acquirer APIs should expose this boundary explicitly rather than abstracting it away.

3. Chargeback: An Issuer-Initiated Dispute and the Costliest Path

A chargeback is not a merchant action at all. It is an issuer-initiated dispute — a formal, rule-governed process through which the issuer forcibly reverses a previously settled transaction on behalf of the cardholder and transfers the liability back to the acquirer.

Chargebacks are governed by the scheme dispute frameworks:

- Visa Dispute Resolution (the successor to the legacy Visa Claims Resolution model).

- Mastercard Dispute Resolution under the Mastercard Transaction Processing Rules.

- Equivalent frameworks at Amex, Discover, JCB, UnionPay, and domestic schemes.

Each framework defines reason codes (e.g., fraud, authorization, processing error, consumer dispute), evidence requirements, response windows, and escalation paths. A chargeback is not a conversation — it is a compliance procedure with timelines measured in days and outcomes measured in liability shifts.

The Lifecycle of a Chargeback

A typical chargeback flow runs 30 to 90 days end-to-end and moves through well-defined stages:

- Cardholder disputes a charge with the issuer (fraud claim, item not received, service not rendered, duplicate billing, authorization dispute).

- Issuer initiates the chargeback through the scheme, assigning a reason code and attaching supporting data.

- Acquirer receives the chargeback and debits the merchant’s settlement account for the disputed amount plus scheme fees.

- Merchant has the option to represent — submit compelling evidence (receipts, EMV authorization data, proof of delivery, CVM evidence) within a defined window, typically 7–45 days depending on scheme and reason code.

- Issuer evaluates the representment and either accepts the defense or escalates.

- Pre-arbitration and arbitration follow if neither party concedes — formal scheme-adjudicated resolution with non-trivial fees and binding outcomes.

Chargebacks Are Not Customer Service

This is the most important point, and the one most commonly misunderstood by merchants, product managers, and even some acquirers: a chargeback is not a customer service mechanism. It is a compliance and fraud escalation path with direct P&L impact.

Every chargeback carries:

- Scheme fees (typically $15–$50 per dispute, regardless of outcome).

- Acquirer processing fees.

- Operational cost to investigate, gather evidence, and represent.

- Chargeback ratio exposure — schemes monitor merchant chargeback ratios, and excessive ratios trigger enrollment in programs like Visa Dispute Monitoring Program (VDMP), Visa Fraud Monitoring Program (VFMP), or Mastercard Excessive Chargeback Merchant (ECM) — each of which carries escalating fines and, ultimately, termination risk.

- Liability transfer — for fraud-coded chargebacks on non-EMV-compliant transactions, the merchant typically absorbs 100% of the loss.

A well-run merchant operation treats refunds as cheap (a few days of capital cost) and chargebacks as expensive (fees, liability, ratio risk, and reputational exposure with the acquirer). The correct architectural posture is to resolve disputes before they become chargebacks — offer refunds proactively, keep EMV and CVM evidence well-preserved for representment, and instrument the customer journey to catch issues before the cardholder calls their issuer.

Quick-Reference Comparison

| Feature | Reversal | Refund | Chargeback |

|---|---|---|---|

| Initiator | Merchant / terminal / acquirer | Merchant | Issuer (on behalf of cardholder) |

| Settlement status | Pre-settlement | Post-settlement | Post-settlement |

| Resolution time | Instant at message level (hours to cardholder) | 2–5 business days | 30–90 days |

| Primary protocol | ISO 8583 MTI 0400 / 0420 | Scheme credit / return transaction | Scheme dispute framework (Visa DR, Mastercard DR) |

| Funds movement | None — hold released | New credit transaction | Forced debit from merchant, credit to cardholder |

| Liability | None — transaction never settled | Merchant bears cost of goods/service | Liability shifts to acquirer/merchant; fees apply |

| Merchant cost | Near zero | Processing fee, capital cost | Scheme fees, representment cost, ratio exposure |

Architectural Implications

For engineers building POS systems, acquirer platforms, or merchant dashboards, these distinctions are not academic. They drive concrete design decisions:

- Terminal software must know the state of the current batch and expose the correct operation (reverse vs. refund) to the merchant UI. Offering “void” as an ambiguous catch-all is a common source of production defects.

- Acquirer APIs should surface settlement status explicitly, so integrators do not attempt reversals against settled transactions or issue redundant refunds against still-pending authorizations.

- Reconciliation systems must treat reversals, refunds, and chargebacks as three distinct financial events with different reporting semantics. Collapsing them into a single “credit” bucket breaks accounting accuracy and masks operational signals — a rising chargeback rate, for example, disappears inside aggregate refund volume.

- Risk and fraud engines should treat chargeback patterns as a first-class signal, separate from refund patterns. A merchant with high refunds and low chargebacks is operating healthily; a merchant with high chargebacks and low refunds is likely mishandling customer contact.

- Customer-facing communication should reflect the underlying mechanism. “Your refund has been issued, and will appear in 2–5 business days” is accurate for a refund and misleading for a reversal, where the hold release may be much faster (or slightly slower, depending on the issuer).

Key Takeaways

The settlement boundary defines the mechanism. Pre-settlement cancellations are reversals; post-settlement returns are refunds; post-settlement disputes are chargebacks.

Reversals are ISO 8583 0400/0420 messages that release authorization holds before batch close. They are instant at the protocol layer, nearly free, and the correct tool whenever the transaction has not yet settled.

Refunds are new credit transactions against an already-settled debit. They traverse the full clearing and settlement cycle and take 2–5 business days.

Chargebacks are issuer-initiated dispute procedures governed by scheme frameworks. They transfer liability, trigger fees, and carry ratio and reputation exposure. They are not a form of customer service.

Architecturally, the three must be modeled as distinct events. Conflating them — in terminal UX, in APIs, in reconciliation, or in reporting — produces predictable classes of operational, financial, and compliance failures.

The cardholder may experience all three as “money coming back.” The payment system does not. Treating the distinction with the precision it deserves is what separates a well-engineered acquiring platform from one that is quietly losing money at the edges.

Further Reading

- What Actually Happens in the 2–3 Seconds of a Card Payment — the full card-present transaction lifecycle, from tap to “Approved”

- Nexo Protocol Adoption in Modern SmartPOS Architectures — how reversals, refunds, and advice messages map from Nexo to ISO 8583

- PIN Translation: Bridging Cryptographic Worlds Inside the HSM — HSM and PIN block handling across the acquirer boundary

- ISO 8583:2003 — Financial transaction card originated messages

- EMVCo — EMV Integrated Circuit Card Specifications, Book 3: Application Specification

- Visa Core Rules and Visa Product and Service Rules, 2024 edition

- Mastercard Transaction Processing Rules, 2024 edition

- Point-of-Sale Systems Architecture: A Practical Guide to Secure, Certifiable POS Systems