This is part 3 of a series on building grounded AI for payment systems. Part 1 made the case that payments need grounded AI, and part 2 Part 2covered the retrieval pattern that delivers the grounding. This post is about where that layer actually earns its keep.

If we want AI to be useful in payments, we need to start with the right question. The question is not “can AI approve or reject a payment?” The question is “can AI help us understand what happened in the payment lifecycle?”

That is where I think the practical value is.

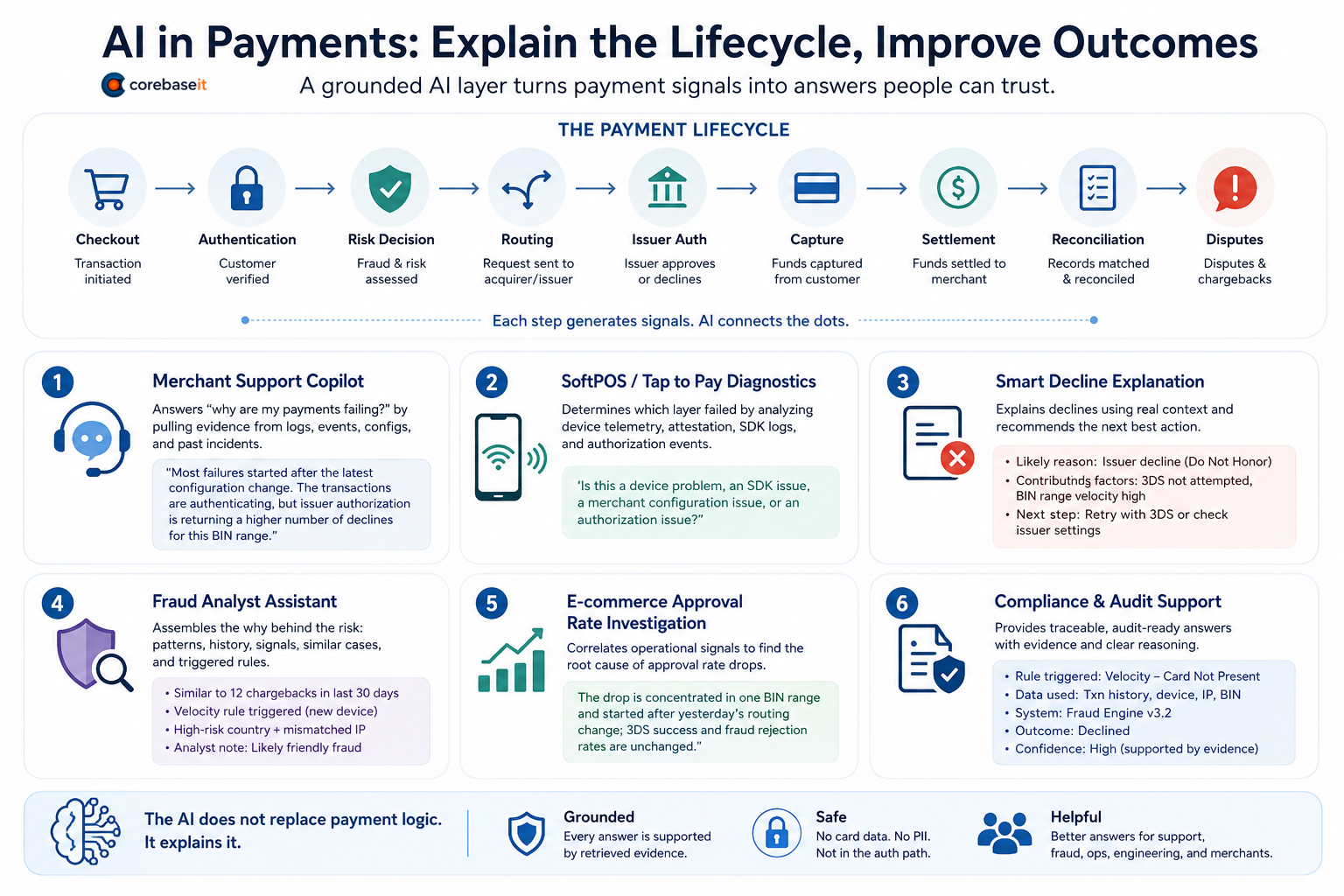

A payment transaction is not a single moment. It is a chain of events: checkout, authentication, risk decision, routing, issuer authorization, capture, settlement, reconciliation, disputes. Each step produces signals, and each signal can explain part of the story. A grounded AI layer, built with retrieval as described in part 2, can put those signals in front of the people who need them. Here are the use cases that make sense to me.

1. Merchant support copilot

A merchant asks: “why are my payments failing?”

Today, answering that means a support agent manually checking logs, transaction events, merchant configuration, and previous incidents across several systems. An AI assistant with retrieval access to those sources can pull the relevant evidence and summarize the likely cause. A grounded answer looks like:

“Most failures started after the latest configuration change. The transactions are authenticating, but issuer authorization is returning a higher number of declines for this BIN range.”

Every claim in that answer points to a record someone can check. That is the difference between a support copilot and a chatbot, and it is measured in resolution time.

2. SoftPOS and Tap to Pay diagnostics

SoftPOS is a strong candidate for this layer because the transaction outcome depends on more than the payment request. The device matters. The SDK matters. NFC availability, device attestation, the PIN flow, and the app version all matter. I covered how much certification weight sits on these components in the L3 certification paths post.

When a Tap to Pay transaction fails, the first question is rarely “why did the issuer decline?” It is “which layer failed?” A grounded assistant that can read device telemetry, attestation results, SDK logs, and authorization events can answer the question support, QA, and engineering teams actually ask:

“Is this a device problem, an SDK issue, a merchant configuration issue, or an authorization issue?”

3. Smart decline explanation

Declines are expensive. They cost revenue, generate support tickets, and erode merchant trust. A payment-aware system can classify and explain declines from the actual context: issuer response, 3-D Secure (3DS) result, fraud decision, routing path, merchant setup, previous attempts, device or checkout errors.

The goal is not to make excuses for the decline. The goal is to identify the most likely reason and the next best action: retry with 3DS, check the merchant configuration, contact the issuer, or escalate to engineering. In a merchant dashboard, that turns a dead-end decline code into a workable instruction.

4. Fraud analyst assistant

Fraud systems already produce scores; I wrote about that pipeline in detecting fraud with AI at the POS. A score alone does not close a case. An analyst still needs to know why the transaction was risky, which signals contributed, whether it resembles previous chargebacks, and whether it fits a known false-positive pattern.

A retrieval-based assistant can assemble that context: the transaction pattern, the merchant history, the velocity signals, similar historical cases, and the rules that triggered. The review gets faster and, just as important, more consistent across analysts.

5. E-commerce approval-rate investigation

When an approval rate drops, the cause is rarely obvious. It could be an issuer, an acquirer route, a 3DS change, a fraud rule, a checkout problem, or a single BIN range. The investigation usually starts with someone pulling data from four systems and building a spreadsheet.

A grounded AI layer can correlate the operational signals and suggest where to look first: “the drop is concentrated in one BIN range and started after yesterday’s routing change; 3DS success and fraud rejection rates are unchanged.” That does not replace the payments team. It gives the payments team a better starting point.

6. Compliance and audit support

In payments, explanations carry obligations. If a system blocks, flags, declines, routes, or reviews a transaction, someone may eventually ask why — a merchant, an auditor, a regulator. A useful AI assistant must be able to answer with evidence: what rule triggered, what data was used, which system made the decision, what the final outcome was, and what remains uncertain.

This is where faithfulness becomes the critical property. The ENWAR evaluation treats faithfulness as a core KPI: every generated claim must be supported by retrieved context, not inferred to fill a gap. For audit-facing answers in payments, I would treat it as a hard requirement. An explanation that cannot be traced back to evidence is not an explanation; it is a liability.

The practical direction

For me, this is the realistic shape of AI in payments. The AI does not replace certified payment logic, does not touch sensitive card data, and does not sit in the authorization path slowing transactions down. It makes the payment lifecycle easier to understand: a grounded intelligence layer for support, fraud, operations, engineering, and merchants.

The payment engine executes. The AI explains. And in complex systems, good explanations are part of reliability.

References

- A. M. Nazar, A. Celik, M. Y. Selim, A. Abdallah, D. Qiao, A. M. Eltawil, “Enwar: A RAG-empowered Multi-Modal LLM Framework for Wireless Environment Perception,” arXiv:2410.18104, 2024.

- P. Lewis et al., “Retrieval-Augmented Generation for Knowledge-Intensive NLP Tasks,” NeurIPS 2020, arXiv:2005.11401.